Office software is closely linked to the PDF,the PDF is also must have to control!

Set home Page Add to Favorites

|

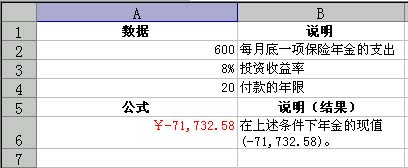

PMT function and based on a fixed rate of interest equal installments, the return of each investment or loan payments. PMT function can be calculated for the repayment of a loan request to pay a certain cycle, when finished, each required to pay the amount of reimbursement that we usually call "installments." For example, by purchase loans or other loans, can calculate the amount of each repayment. The form of its syntax: PMT (rate, nper, pv, fv, type) which, rate for the period of interest rate is a fixed value, nper for a total investment (or loan), that the investment (or loan) the payment of the total period shall, pv is the present value, or a series of future payments and the current cumulative value, also known as the principal, fv values for the future, or the last payment in the hope that the cash balance, if omitted fv, the the assumption that its value is zero (for example, a loan that is the future value of zero), type is 0 or 1, for the designated time period for payment in the beginning or end. If you omit the type, then the assumption that its value is zero. For example, the need for 10 months to pay the annual interest rate of 8% �� 10,000 loan amount of the monthly support: PMT (8% / 12,10,10000) calculated as follows: - �� 1037.03. (D) for the present value of an investment in PV PV function used to calculate the present value of an investment. The present value of annuity is the future phases of the value of an annuity is the sum of. If the current value of the investment recovery is greater than the value of the investments, then the investment is profitable. Its grammatical form: PV (rate, nper, pmt, fv, type) of which the interest rate Rate for the period. Nper for a total investment (or loan), that the investment (or loan) the total number of payment period. Pmt for the period amount to be paid, and its values remain unchanged during the entire annuity. Pmt usually include principal and interest, but does not include other fees and taxes. Fv value for the future, or after the last payment of the cash balance would have liked, if omitted fv, is the assumption that its value is zero (the future value of a loan that is zero). Type used to specify the time period for payment in the beginning or end. For example, suppose an insurance policy to purchase an annuity, the insurance can be in the next two decades at the end of the return �� 600 per month. The cost of the annuity purchase 80,000, assuming an investment return of 8%. Then the present value of the annuity for: PV (0.08/12, 12 * 20600,0) calculated as follows: �� -71732.58. Negative that it is a payment, that is, expenditure on cash flow. Annuity (�� -71732.58) is less than the present value of the actual payment of the (�� 80,000). Therefore, it is not a cost-effective investment.

|